The Widower

Mailings and Financial Matters Suggest Cheryl Lives On

Two years ago this month, my dear wife, Cheryl, died of Alzheimer’s complications after battling the disease for a decade. Still, mailings and financial matters tied to Cheryl persist. They leave me shaking my head.

In recent weeks, I’ve received:

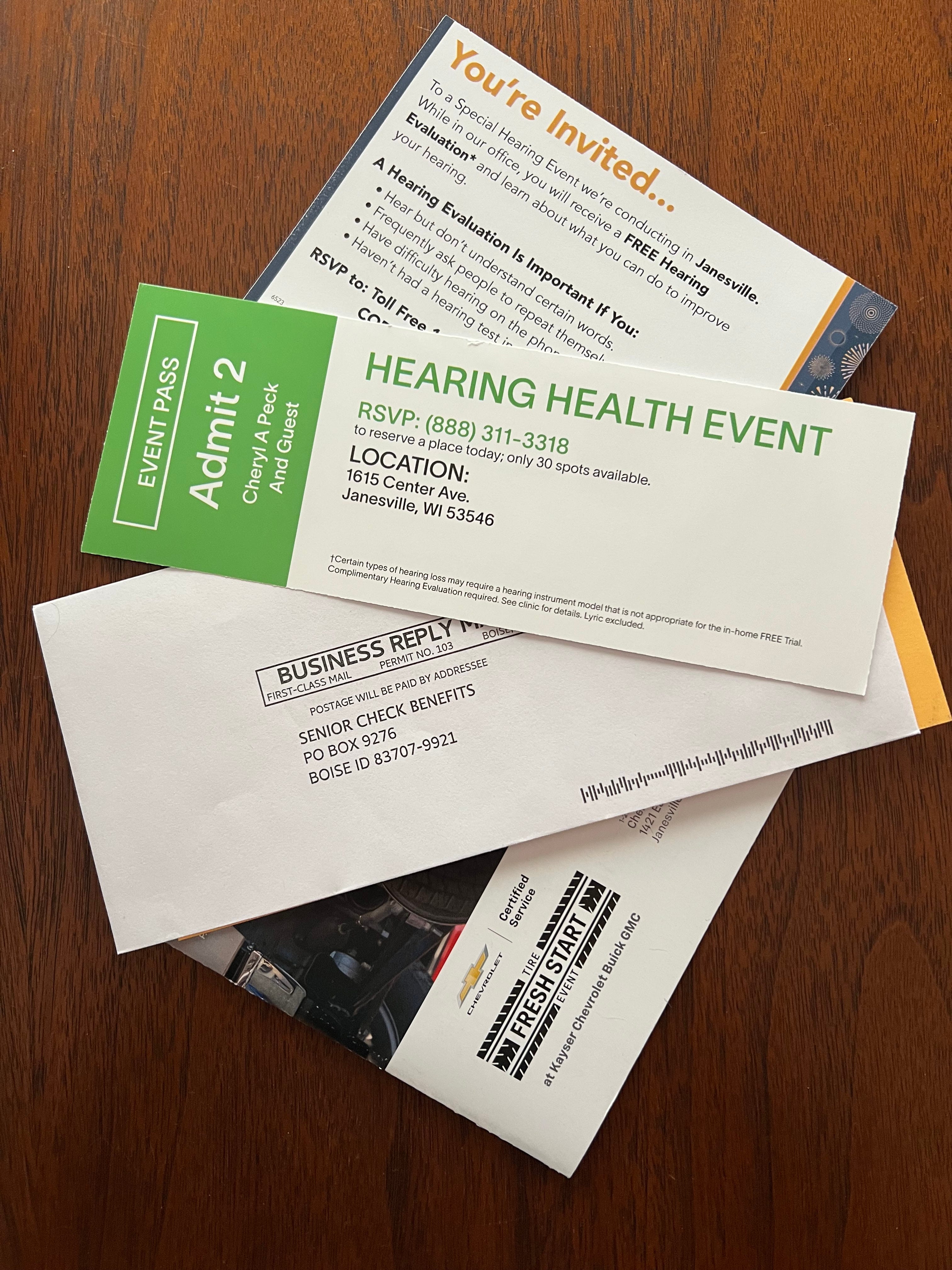

--A solicitation—with ticket for Cheryl Peck and guest—to attend a hearing health event here in Janesville, Wisconsin. I don’t think a hearing aid is in her future.

--A pitch from a local athletic club—one in which she was a member and I still am—for Cheryl to sign up before a rate increase. She won’t be.

--“Spaces are limited,” sounded the alarm for yet another hearing aid event in Janesville, this one using Cheryl’s previous married name.

--A promotion from AARP for auto insurance through The Hartford urged Cheryl to request a free quote today. Needless to say, she doesn’t drive anymore.

--A “fresh start” tire advertisement for Cheryl from an auto dealer. (See auto insurance needs, above.)

--A travel brochure urging Cheryl Peck to book a Viking cruise. I wonder how she’d use the $500 shipboard credit.

--A form from Senior Check Benefits for Cheryl to fill out and see if Social Security will pay up to $255 for her funeral and final expenses. That one was a gut punch. Should I send it back suggesting their pitch is two years too late?

--A pitch from our bank suggesting Cheryl could earn up to $560 in cash bonuses and rewards by opening “a checking and savings account that make (sic) your life simpler.” Oddly, this one also used her previous married name.

You’d think that artificial intelligence, the grand technology we hear about daily, would eliminate senseless mailings. But then, when a friend had me speak about my bird photography at a holiday party and used an AI site’s analysis to introduce me as a retired journalist and author, he knowingly skipped the part stating that I still lived with my wife.

As I explained in a subsequent Facebook post, that AI site had other errors, too. When I later googled “Greg Peck, author, journalist, Janesville, Wisconsin,” I likewise found errors, including that I supposedly authored a fourth book that I know nothing about. A later recheck found changes, but that synopsis suggested one of my books is “a true crime narrative” (my first book involves a tragedy, not a crime), and the accompanying photo wasn’t me!

Our bank’s home equity loan monthly statements are still addressed to “Gregory and Cheryl Peck,” even though many top employees know Cheryl died. Is it my responsibility to request paperwork withdrawing her name from an account on which neither of us has ever taken out a loan? I’m not sure it matters that her name is still on it, so I haven’t bothered.

Which brings me to two other financial matters. I made several attempts to alert a magazine that Cheryl had died. First, I ignored the fact that the publication kept coming, figuring the subscription would soon expire. However, the company kept sending notices that her subscription was about to expire and urging urgent action. Being an environmentalist, I wondered how many trees were dying in these mailings. So I invested a stamp and mailed one back stating she was deceased and signing my name.

That didn’t help. Finally, I tracked down an email address for the magazine and explained. A few weeks ago, I received a refund for the remainder of Cheryl’s subscription, a grand total of $1.67, made out to “The Estate of Cheryl Peck.”

At (our) my bank, a young female teller, after fending off the interests of the tall young man in line ahead of me, told me the only way she could cash it was if I opened an account for “The Estate of Cheryl Peck.”

“I’d rather shred it than go through all that,” I replied.

This month, I received an even bigger “refund”—$248.85 from Wisconsin Power & Light. Huh, I thought. We use Alliant Energy. A computer search told me they’re one in the same. I called and a woman told me it was a legitimate refund for some apparent excess or duplicate payment.

“That’s strange. My wife died 23 months ago, and that’s when I switched the account to my name.”

The woman had no explanation why a refund from when Cheryl was alive took so long to reach me.

“I hope my bank will cash it,” I told her.

Taking both checks—biggie and puny—to the main branch downtown, where people know me, I was steered to the bank manager, who was at a teller window. She agreed to cash both as long as I deposited them and understood that ensuring they clear might take a week.

I shouldn’t be alarmed that a utility refund took two years to reach me. She once cashed one for $800 that took eight years to reach the family.

Cheryl handled all the bill payments until dementia caught up with her and I discovered she paid two phone bills one month because she forgot to pay the previous month, and she let our auto insurance lapse due to nonpayment.

That banker’s story about a refund coming eight years late leaves me wondering what my future might hold.

Wow, spot on Greg. I can 100% relate to everything you touched on, from utility to bank statements to Advertisment offers, that there's no way my husband could take them up on. As he passed 10 months ago. So frustrating!

For Pete's Sake!